Founded by Mehrteab Leul Kokeb, and a leading full-service law office in Ethiopia, and has over 20 years experience advising and representing clients on wide range of legal issues concerning business and investment in the country.

Friday, 09 September 2022 08:22

Legal Update on Limit on Foreign Currency Holding in the Territory of Ethiopia

Written by Mehrteab Leul & Associates

Introduction

The National Bank of Ethiopia (NBE) has introduced a Limit on Birr and Foreign Currency Holding in the Territory of Ethiopia Directive (“New Directive”) which repealed and replaced the previous directive regulating the matter, Directive No. FXD/49/2017, effective from September 5, 2022. We have prepared this short legal update to give our clients an overview of the main change brought by the New Directive.

On Foreign Currency Holding and Timeline Limit for Incoming Individuals (through air transportation)

Resident person in Ethiopia entered into the territory of Ethiopia should convert all the foreign currency they hold at authorized forex bureau or deposit to their foreign currency account, if they have, within one month from the date of entry. If the amount exceeds US$ 4000, they have to present customs declaration.

Diasporas and Ethiopian who are non-resident and intended to stay in Ethiopia for more than three months should transfer all the foreign currency they hold to their non-resident foreign currency account or foreign exchange saving account within three months from the date of entry. If the amount exceeds US$ 10,000, however, they have to present custom declaration.

Foreigners who are not residing in Ethiopia can hold the amount of foreign currency they hold without restriction until the expiration of their visa.

On Foreign Currency Holding and Timeline Limit for Outgoing Individuals (through air transportation)

A person residing in Ethiopia can travel aboard with foreign currency purchased from the bank within one month from the date of a bank advice. Non-resident diaspora and Ethiopian nationals who are not residing in Ethiopia can travel aboard with foreign currency either purchased from the bank within one month from the date of a bank advice or if they enter the country and leave within three months. If the amount exceeds US$ 10,000, they have to present customs declaration.

Embassy and international institutions’ employees, trainers and workshop participants who enter the country can hold more than US$ 10,000 if they provide either bank advice or employer’s letter or supporting letter that justify the acquisition of the foreign currency is from a legal source.

On Foreign Currency Holding and Timeline Limit for Incoming Individuals (through inland transportation)

A person entering into the territory of Ethiopia through in land transportation should declare at the board if they hold other foreign currency which have equivalent or more than US$ 500.

On Birr Holding Limit for Incoming and outgoing Individuals

Any person entering to and departing from Ethiopia can hold up to ETB 3000 per travel. However, travel from and to Djibouti can hold up to a maximum amount of ETB 10,000 per travel.

On Prohibited Transactions

Unless as provided in this New Directive or other laws, it is prohibited to hold foreign currency. It is also prohibited to undertake any transaction in foreign currency. Therefore, the New Directive prohibits to pay foreign currency in cash to a third party either to discharge a contractual or other obligations or by way of gift and/or donation unless as provided the New Directive, other laws or without prior authorization of the NBE. Any person who acquired foreign currency by means of donation and/or gift before the coming into effect of the New Directive should convert the currency s/he received to Ethiopian birr within one month therefore until October 05, 2022.

Disclaimer: This information is intended as a general overview and discussion of the subjects dealt with. The information provided here was accurate as of the day it was posted; however, the law may have changed since that date. This information is not intended to be, and should not be used as, a substitute for taking legal advice in any specific situation. Mehrteab & Getu Advocates LLP is not responsible for any actions taken or not taken on the basis of this information. Please refer to the full terms and conditions on our website.

Copyright©2022 Mehrteab & Getu Advocates LLP. All rights reserved.

Thursday, 18 August 2022 13:16

Legal Update on the New Council of Minsters Regulation to provide for Social Welfare Levy on Imported Goods

Written by Tibebe Zewdu

Introduction

The Federal Council of Ministers in its 10th regular session held on 06 August 2022 has introduced a Regulation that imposes Social Welfare Levy on imported goods which will be in force upon official publication of the Regulation in the Federal Negarit Gazette.

The Purpose and Content of SWL Regulation

The commonly applicable taxes on imported goods in Ethiopia include: Customs Duty, Excise Tax, VAT, Surtax, and Withholding tax. Given the urgency to increase fiscal space to enable the rehabilitation and construction of conflict-ridden regions, the government is working on increasing tax revenues, hence - the introduction of this Social Welfare Levy. The purpose of the Social Welfare Levy is therefore “to fulfil the commitment of the Government to provide and finance education, health and other social services.”

The Social Welfare Levy would be levied and collected on all types of goods imported into the country save for persons and organizations with diplomatic privileges and goods that are subject to surtax as per the Import Sur-Tax Regulation No. 133/2007.

The Levy would be collected at the rate of 3% of the aggregate cost, insurance and freight (CIF) value of the goods rather than on the value of the goods. This resembles the 3% Withholding Tax that is currently paid on goods imported for commercial use. Accordingly, other payable duty and taxes on imported goods such as Customs Duty, Excise tax, VAT and Surtax will not be taken into account to form the basis for computation of the Social Welfare Levy.

Disclaimer

The information contained in this legal update is based on the draft regulation. The official Regulation is yet to be published on Federal Negarit Gazette. The information is for general information purposes only. Nothing in this legal update is intended as legal advice.

Tuesday, 16 August 2022 16:02

Legal Update on the new Council of Ministers Regulation to amend the Federal Income Tax Regulation

Written by Tibebe Zewdu

Introduction

The Federal Council of Ministers has resolved in its 10th regular meeting held on 06 August 2022 to amend the existing Income Tax Regulation by adding share premiums as an additional item of exempt income. Although this amendment will take full effect upon its official publication in the Federal Negarit Gazette, we have prepared this update to give our clients an overview of what this amendment holds.

Exemption of Premium Income

The existing Income Tax Regulation No. 410/2017 (as amended) already has a list of incomes that are exempted from tax. The recent resolution by the Council of Ministers adds one important item to this list of exemptions on share premium, which is defined by the Ethiopian Commercial Code as the difference between the par value and the selling price of newly issued shares.

The status of tax on income generated by way of issuing new shares at a premium was not clear until the Ministry of Finance came up with the Capital Gains Tax Directive no. 8/2011 (hereinafter “the Directive”) which was effective from the 7th of August 2019, indicating that income derived by any company from the issuance of new shares in excess of the par value would be subject to income tax at the rate of 30%.

As per the amendment, “premium income obtained by going concerned from the sale of new shares to non-residents will be exempted from income tax”. By doing so, the amendment repeals what is stated in the Directive. For the income to be qualified for exemption under this amendment, it has to fulfill three cumulative elements.

First and foremost, the income should be the result of the sale of newly issued shares by a company rather than the sale of existing shares by the shareholders. The latter is not included under the exemption. The second requirement is that the issuance of new shares should be issued by a company that has the potential of continuing in the business for a foreseeable period. The last yet very important element is that the exemption is only applicable if the buyers of the new shares are non-residents. Although the rationale for excluding resident entities from the exemption is not clear and could be seen as going against the principle of tax neutrality, the preamble to the amendment resolution indicates that economical reason is the main objective for the amendment by way of increasing foreign direct investment in local companies in the form of share premiums.

Disclaimer:

The information contained in this legal update is based on the draft amendment. The official Regulation is yet to be officially published on Federal Negarit Gazette. The information is for general information purposes only. Nothing in this update is intended as legal advice.

Copyright©2022 Mehrteab & Getu Advocates LLP. All rights reserved.

Thursday, 27 January 2022 10:37

The National Bank of Ethiopia’s New Directive on Retention and Utilization of Foreign Currency Earnings from Export and Inward Remittance (06 January 2022)

Written by Mehrteab Leul & Associates The National Bank of Ethiopia (“NBE”) issued a new directive (Directive No. FXD/79/2021) governing the retention and utilization of foreign currency earnings from export and inward remittance. Previously the area was regulated by the Directive No. FXD/73/2021 (“Old Directive”). In this edition of our legal update, we have tried to look in to the changes introduced by the New Directive preceded by a highlight on the changes made by the series of directives of NBE governing the area.

The National Bank of Ethiopia (“NBE”) issued a new directive (Directive No. FXD/79/2021) governing the retention and utilization of foreign currency earnings from export and inward remittance. Previously the area was regulated by the Directive No. FXD/73/2021 (“Old Directive”). In this edition of our legal update, we have tried to look in to the changes introduced by the New Directive preceded by a highlight on the changes made by the series of directives of NBE governing the area.

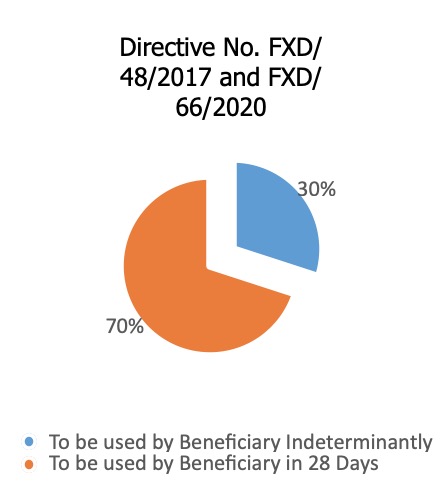

For three years, this part of the foreign currency management regimes of NBE was regulated by the Retention and Utilization of Export Earnings and Inward Remittance Directive No. FXD/48/2017 that entered in to force on 3 October 2017 and was effective until replaced by the Retention and Utilization of Export Earnings and Inward Remittance Directive No. FXD/66/2020 that entered in to force as of the 16 September 2020. The later Directive introduced minor changes regarding credit of funds in retention accounts for local merchants or entities licensed by NBE and the manner of using foreign currency available in Retention account A and B. Under both these directives, an exporter or a foreign currency remittance beneficiary had the right to maintain 30% of the foreign currency earnings in Retention Account A for indefinite period of time and the remaining 70% would be retained in Retention Account B for a period of 28 days and before the lapse of the 28 days it was possible to use the currency for importing specified items.

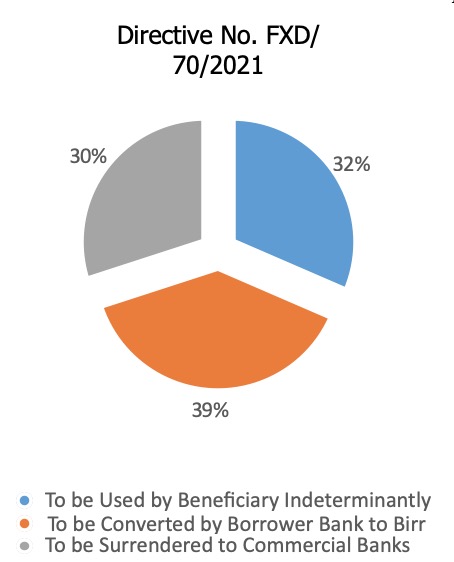

NBE issued Directive No. FXD/70/2021 by repealing Directive No. FXD/66/2020. Directive No. FXD/70/2021 entered in to force as of 09 March 2021. This Directive brought about significant changes by, among others, eliminating the Retention Account “A” and Retention Account “B” and recognizing only one Forex Retention Account, establishing a mandatory surrender requirement where all the beneficiaries are required to surrender 30% of the foreign currency earning to NBE, and reduced the amount of proceeds to be retained in the retention account to 45% (of the remaining currency after the surrender) and it required the sale of 55% (of the remaining currency after the surrender) of the foreign currency earning to the banks immediately on the day of receipt at the prevailing buying exchange rate. It also changed the requirements for utilization of the foreign currency permitting beneficiaries to use the foreign exchange for the importation of goods and services without restriction as long as it has a business license to import these goods and services.

NBE issued Directive No. FXD/70/2021 by repealing Directive No. FXD/66/2020. Directive No. FXD/70/2021 entered in to force as of 09 March 2021. This Directive brought about significant changes by, among others, eliminating the Retention Account “A” and Retention Account “B” and recognizing only one Forex Retention Account, establishing a mandatory surrender requirement where all the beneficiaries are required to surrender 30% of the foreign currency earning to NBE, and reduced the amount of proceeds to be retained in the retention account to 45% (of the remaining currency after the surrender) and it required the sale of 55% (of the remaining currency after the surrender) of the foreign currency earning to the banks immediately on the day of receipt at the prevailing buying exchange rate. It also changed the requirements for utilization of the foreign currency permitting beneficiaries to use the foreign exchange for the importation of goods and services without restriction as long as it has a business license to import these goods and services.

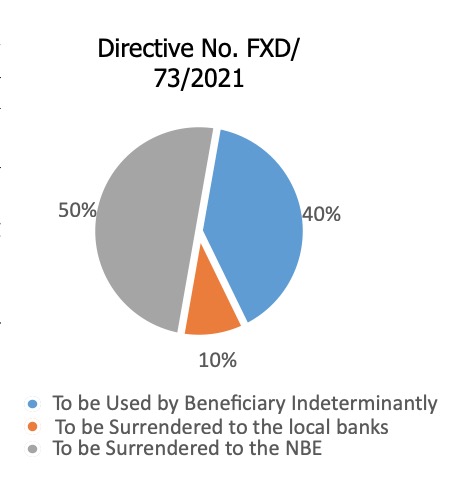

Effective from 01 September 2021, NBE repealed Directive No. FXD/70/2021 and issued Directive No. FXD/73/2021 governing the retention and utilization of foreign currency earnings from export and inward remittance. This Directive introduced 50% - 40% - 10% allocation requiring exporters and remittance earners to surrender 50% of their total earnings to NBE, permitted the account holders to retain 40% of the foreign currency earning indefinitely and sale the remaining 10% to the commercial banks.

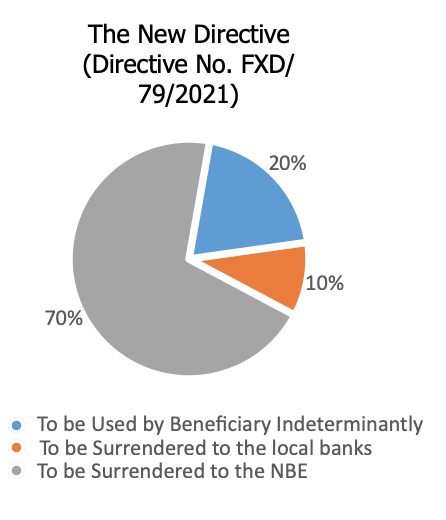

Directive No. FXD/73/2021 is a short lived one as NBE replaced it by a New Directive (Directive No. FXD/79/2021(“New Directive”)) that takes effect from 06 January 2022. The basic changes introduced by this New Directive are:

Total surrender amount is increased: Under the New Directive, exporters and inward remittance earners are required to surrender 70% of their total earnings to NBE. Previously, exporters and inward remittance earners were required to surrender 50% of their total earnings to NBE.

Total surrender amount is increased: Under the New Directive, exporters and inward remittance earners are required to surrender 70% of their total earnings to NBE. Previously, exporters and inward remittance earners were required to surrender 50% of their total earnings to NBE.

Amount of proceeds to be retained is significantly decreased: Under the Old Directive, retaining 40% of the total foreign currency earning for indeterminate period of time in a retention account was permitted after deduction of the 50% surrender requirement. The remaining 10% of foreign currency amount was required to be surrendered to the respective commercial banks based on the prevailing exchange rate and using the buying rate. Under the New Directive, the amount of foreign currency to be surrendered has increased significantly. Commercial banks are required to surrender 70% of the total foreign currency earning from export and remittance earnings to the NBE. The remaining 10% of the foreign currency amount is required to be surrendered to the respective commercial banks based on the prevailing exchange rate and using the buying rate.

Simply put, the New Directive changed the allocation to 70% - 20% - 10% (70 percent to NBE, 20 percent to the retention account for the benefit of exporters and inward remittance earners and 10 percent to commercial banks).

Simply put, the New Directive changed the allocation to 70% - 20% - 10% (70 percent to NBE, 20 percent to the retention account for the benefit of exporters and inward remittance earners and 10 percent to commercial banks).

Disclaimer: This information is intended as a general overview and discussion of the subjects dealt with. The information provided here was accurate as of the day it was posted; however, the law may have changed since that date. This information is not intended to be, and should not be used as, a substitute for taking legal advice in any specific situation. Mehrteab Leul & Associates is not responsible for any actions taken or not taken on the basis of this information. Please refer to the full terms and conditions on our website.

Copyright©2022 Mehrteab Leul & Associates. All rights reserved.

Monday, 25 October 2021 07:51

Key Changes Introduced by the Amendment of the Federal Income Tax Regulation No. 410/2017

Written by Mehrteab Leul & Associates

Introduction

The Council of Ministers has amended some provisions of the Federal Income Tax Regulation No. 410/2017 (“Regulation”) on September 23, 2021. The amendment was said to be necessitated by the reason that some provisions of the Regulation lack clarity and impacted economic transactions. The amendment (“Amendment”) has the aim of enabling the tax authority collect taxes by resolving the disagreement between the tax authority and taxpayers caused by lack of clarity on the Regulation. It has also the aim of increasing the flow of investment through amending those provisions that adversely impact investment. We have summarized the basic changes introduced by the Amendment as follows:

Depreciation allowance is permitted for lessees in a hire-purchase arrangement

Under the Capital Goods Business Proclamation No, 103/1998, three types of capital goods leasing are recognized i.e. finance lease agreement, operating lease and hire-purchase lease agreements. The Regulation provides a uniform treatment for all kinds of lease arrangements whereby the rent paid by the lessee would be a deductible expense. However, given the fact that in a hire-purchase arrangement, the lessee would be the owner of the leased property after settling all the rent, the Amendment permits these lessees to have depreciation allowance on the leased property instead of treating the rent as a deductible business expenditure.

No depreciation allowance is permitted for a building which is not completed even though partially used as a business asset

The provision of Article 40 of the Regulation was ambiguous in relation to allowing depreciation for buildings partially used as a business asset. The Amendment makes it clear that only buildings that are completed would be entitled to a depreciation allowance in proportion to the portion of the building used as a business asset, if the buildings are used partially as business assets and partially for other purposes.

Loss-carry forward benefit is applicable only if the taxpayer has a taxable income

The Amendment has provided that if the taxpayer has incurred a loss for more than one tax year, the loss of the earlier year must be deducted first. In this regard, the loss will be deducted only if the taxpayer has a taxable income. The loss cannot also be forwarded beyond a period of five years.This is apparently aimed to resolve the contention that a taxpayer who has incurred a loss for more than one year must be entitled to a loss carry-forward privilege for a period of more than five years.In addition, the Amendment has endowed the Ministry of Finance the discretion to allow a third loss suffered by a taxpayer engaged in the manufacturing sector to be carried forward when it believes that there is good cause for doing so.

The treatment of foreign exchange loss has been changed

The Regulation used to provide that if a taxpayer has incurred a foreign currency exchange loss, this loss would only be offset against a foreign currency exchange gain derived by the taxpayer. However, this provision was found to be problematic as most investors and business entities usually do not come across a foreign currency gain. The Amendment changed this and provided that if the foreign exchange loss was sustained in relation to the purchase of capital goods, the loss will be added to the cost of the capital good to be used as a basis for calculation of depreciation. On the other hand, when the loss is incurred for operating expenses, the loss will be considered as a deductible expenditure for the tax year.

Adjustment of Inflation is permitted for shares and bonds in the calculation of capital gains tax

Under Ethiopian income tax law, transfer of immovable properties and shares bonds is subject to Capital Gains Tax. In calculation of such tax, the Regulation allowed inflation adjustment to be made only in respect of the transfer of immovable assets. Now, under the Amendment, inflation adjustment is also permitted to be made to the cost of shares and bonds.

Continued application of the previous Income Tax Proclamation No. 286/2002 for losses carried forward under the same Proclamation

There were occasional arguments on part of some taxpayers that they should be entitled to a new set of loss-carry forward privilege after introduction of the currently applicable Income Tax Proclamation in substitution of the old one. But the Amendment now provides that taxpayers who have carried forward two losses under the previous Income Tax Proclamation will not be entitled to carry-forward any further losses under the new Income Tax Proclamation. If the taxpayer has any loss that should be carried forward under the repealed Proclamation, the loss carry forward will be treated under that law. This means, if the taxpayer has carried forward a loss for one tax year under the repealed proclamation, it will be entitled to carry the remaining loss forward in accordance with the repealed Proclamation. This is to emphasize that the taxpayer is entitled for a loss-carry forward privilege for not more than two losses sustained in its lifetime.

Retroactive application of the Amendment

The Amendment is made to be applicable to outstanding tax disputes and controversies that have not yet been resolved. Accordingly, all tax arrears that emanate from the aforementioned amendments would be settled in accordance with the Amendment.

Disclaimer: This information is intended as a general overview and discussion of the subjects dealt with. The information provided here was accurate as of the day it was posted; however, the law may have changed since that date. This information is not intended to be, and should not be used as, a substitute for taking legal advice in any specific situation. Mehrteab Leul & Associates is not responsible for any actions taken or not taken on the basis of this information. Please refer to the full terms and conditions on our website.

Copyright©2021 Mehrteab Leul & Associates. All rights reserved.

MLA is pleased to announce its seedlings planting initiative with focus on post planting care for the seedlings. With the shared view of building responsibly grounded business in Ethiopia, MLA is proud to collaborate with its valued corporate clients in this noble imitative.

Wednesday, 26 May 2021 13:03

The Ethiopian Investment Commission’s New Directive on Work Permits for Expats and Knowledge Transfer from Expats to Ethiopians

Written by Benyam Tafesse

I. Scope and Purpose

With the aim of creating a one stop service for investors, the Ethiopian Investment Commission has recently issued a Directive Regulating the Issuance of Work Permit to Expats Employed in Investments and the Implementation of Knowledge and Skill Transfer from Expats to Ethiopians (Directive No. 772/2021 hereinafter ‘the Directive’ ). The Directive seeks to regulate the employment of expats in those investment enterprises that fall within the administrative mandate of the Commission. As such, whilst the Expat Work Permit Directive (Directive No. 23/2018) that was issued by the Ministry of Labour and Social Affairs will continue to regulate the employment of expats in other sectors of the economy, the Directive seeks to regulate the employment of expats in wholly foreign owned investments, joint investments that are made between domestic and foreign investors, investments made by foreign nationals who are treated as a domestic investors, and investments made by domestic investors in those areas that are eligible for incentives.

The Directive also seeks to regulate the employment of refugees who hold a valid identity paper and are seeking to engage in wage employment in Ethiopia. However, the Directive does not regulate the employment of refugees in rural and urban investment projects that have been jointly designed by the Ethiopian government and the international community with the intention of benefiting refugees.

II. Top Management and Impermanent Non-management Positions

As with the previous directive issued by Ministry of Labor & Social Affairs, the Directive allows an investor to employ foreigners for top management positions in either the construction or implementation phases of a given investment project without any restriction and without the need for complying with preconditions set for other expats - particularly in relation to positions that can be filled by Ethiopians and duties pertaining to knowledge and skill transfer

In relation to impermanent non-management positions, the new Directive has laid out clear instructions that regulate the number of expats that can be employed and the duration of such an employment during the investment project’s construction, installation, commissioning, implementation and maintenance phases. In this respect, although a company is not expected to explore the availability of Ethiopians before hiring expats for management and impermanent non-management positions, they are expected to set up and provide on-the-job training in order to replace such expats with Ethiopians within a defined period of time.

III. Other Positions within the investment enterprise

In relation to positions that are neither top management nor impermanent non-management positions, the Directive has a separate process for the validity and renewal process of work permits. In this regard, whilst a work permit to be provided to expats for such positions are valid for only one year and such work permits cannot be renewed for more than three years, the Directive provides an exception for these requirements in compelling or necessary conditions and in cases where a company has invested a capital of at least 40 million USD or hired more than one thousand five hundred employees.

Furthermore, the Directive barres a company from assigning a new expat employee to such positions on which a foreigner had previously served for three years. However, the Directive provides an exception from this requirement when it is unequivocally demonstrated through evidence that the transfer of knowledge and skill was not properly implemented for reasons not attributable to the company, or because the trained Ethiopians left the company on their own will, or the contract of employment was terminated through the fault of the trainee employee.

Similarly, according to the Directive, the renewal of a work permit may only be approved only if it is proven that the enterprise has executed the training of Ethiopian replacements appropriately. However, a work permit may also be renewed without such requirement when it is proved by the Commission that the expat is relevant for the position and that the particular work is of a continuous nature.

IV. Knowledge and Skill Transfer

A key aspect of the knowledge transfer scheme in the Directive is the obligation of employers to develop a program that clearly outlines not only the timeline for the replacement of expat employees, but also the nature and schedule of such training. In this regard, the employer is mandated to submit quarterly performance reports of trainings that have been offered or due to be offered by the employer. The Directive also requires that the first-round training program that is to be prepared by the employer shall, at the latest, be presented within one week from the date of employment of the expat.

Furthermore, given the importance of knowledge transfer schemes, the Directive also empowers the Commission to conduct field monitoring every three months in order to assess the implementation and effectiveness of those on-the-job trainings that are being offered to Ethiopians. Beyond these obligations, the employer is also expected to notify the Commission in writing, within 5 working days, if the expat either leaves their place of work, if their employment contract is either terminated or has ended, or if the address of the workplace has changed.

V. Expat Obligations

The Directive also imposes certain obligations on the expats in relation to fulfilling requirements related to their employment. For example, the Directive states that the employee must appear at a workplace in possession of the issued work permit, must adhere to those procedures that seek to transfer standard knowledge and skill to Ethiopian replacements and comply with the Commission’s request for reporting. Furthermore, the employee is expected to only work for the employer specified in the work permit, refrain from engaging in illegal and immoral activities and only engage in the position/profession registered in the work permit.

Given that failing to comply with the employer and employee obligations that are prescribed under this Directive will result in the revocation of the work permit, it is in the best interest of both parties to not only adhere to their respective obligations, but to also ensure that the particular implementation and supervision criterions listed in articles 5, 6, 9 and 10 of the Directive are understood, respected and observed.

Monday, 10 May 2021 06:10

Legal Update: Highlights Of Key Changes And Introductions Made By The New Arbitration And Conciliation Proclamation

Written by Mehrteab Leul & Associates

INTRODUCTION

Ethiopia did not have an independent piece of legislation that regulated the manner in which alternative means of settling disputes operate. It was only the Ethiopian Civil Procedure Code and the Ethiopian Civil Code (“Previous Laws”), together with other scattered provisions in various laws, which used to regulate arbitration and conciliation for over half a century. These laws provided for basic frameworks of conducting arbitration and conciliation such as governing the arbitration agreement, manner of composition of tribunals, and the arbitration award. However, these laws were criticized for failing to sufficiently address, among other things, the manner of establishment and operation of arbitration centres, identifying arbitrable and non-arbitrable matters, providing a limitation on the role of courts during the arbitration proceeding, the appealability of arbitration awards and the competency of the arbitration tribunal to decide on its own jurisdiction. The provisions under the Previous Laws are also highly incompatible with the internationally recognized principles of commercial arbitration.

The dispute settlement mechanism prevailing in the country is litigation, more than any other, as the litigation system is characterised by protracted lawsuits that take years to resolve a matter. This has inevitably resulted in a congested court environment. However, this system does not go along with the very nature of commerce for which time, predictability and confidentiality are of the essence; features which are not exhibited in the Ethiopian litigation system.

As part of the recent legislative reform the country is undertaking, the Ethiopian House of People’s Representatives recently ratified the new Arbitration and Conciliation Proclamation No.1237/2021 (the “Proclamation”). The Proclamation entered in to force on 02 April 2021. It basically repealed and replaced Articles 3318-3324 of the Civil Code, which governed conciliation, and Articles 3325 to 3346 of the Civil Code, which governed arbitration. The provisions of the Civil Procedure Code from Articles 315 to 319 and Articles 350, 352, 355-357 and 461, which deal with arbitration, have also been repealed by the Proclamation.

With the aim of complementing the right to justice and to contribute to the resolution of investment and commercial disputes and to the development of the sector, the Proclamation recognized the fact that arbitration and conciliation help in rendering efficient decisions by reducing the cost of the contracting parties, protecting confidentiality, allowing the participation of experts and the use of simple procedure which provides freedom to contracting parties. It also aims to provide for a general framework for the identification of arbitrable cases, management of arbitration proceedings and execution of those decisions that fit the prevailing reality of Ethiopia. By amending the existing laws, the Proclamation aims to be in line with the international principles and practice and support the implementation of international treaties.

Under this piece of MLA’s Legal Update, we will highlight the key changes and introductions made by the Proclamation as follows.

ARBITRATION

Scope of Application: The Proclamation regulates arbitration and conciliation modes of dispute settlement. It is primarily applicable to commercial related national arbitrations, international arbitrations with a seat in Ethiopia or outside Ethiopia and national conciliation proceedings. The Proclamation is also applicable when one of the contracting parties is situated in Ethiopia and where the place of arbitration is not designated.

Definition of International Arbitration: Unlike the Previous Laws, the Proclamation provides a clear and exhaustive definition of what international arbitration constitute. The arbitration would be considered as international when the parties agreed, in express terms, that the subject matter of the arbitration agreement relates to more than one country, when the principal business of the contracting parties is in two different countries at the time of conclusion of contract, where the chosen place of arbitration or the place of performance or the place of business of the subject matter of the dispute arises or is closely connected with a foreign country. Defining international arbitration is relevant to determine the applicable substantive laws and to ensure the independence of a sole-arbitrator who shares nationality with one of the parties to the arbitration.

Prohibition of Court Intervention: As a basic departure from the Previous Laws, the Proclamation introduced a prohibition on the intervention of courts in the arbitration proceeding. The Proclamation specifically mentions some exceptions where the courts may intervene in the arbitration proceeding.

Electronic Arbitration Agreement: In line with the Electronic Transaction Proclamation No.1205/2020 and other laws that recognize electronic communications as a valid means of creating a contract, the Proclamation recognizes that an arbitration agreement can be made by the parties to the contract using electronic communication. Electronic agreements include agreements made through electronic media and accessible for subsequent use.

Definition of Non-Arbitrable Matters: As another basic departure from the Previous Laws, the Proclamation contains an illustrative list of matters which are not subject to arbitration. Previously, it was not clear which matters are arbitrable and which are not. Matters relating to family such as divorce, adoption, guardianship, tutorship and succession cases, criminal matters, tax matters, judgement on bankruptcy and dissolution of business organizations, land matters, administrative contracts unless permitted by law, trade competition and consumer protection related matters, administrative disputes and other matters made non arbitrable by other laws are not arbitrable matters under the Proclamation and the parties cannot agree to settle those disputes by way of arbitration. In fact, the Civil Procedure Code used to take administrative contracts out of arbitration agreement and this is maintained under the Proclamation.

Applicable Substantive Law: The Proclamation gives freedom to the parties when choosing the applicable substantive law. However, in the case when the arbitration seat is in Ethiopia, the applicable substantive law will also be Ethiopian law when the parties have not chosen the applicable law.

Composition of Arbitration Tribunals: the Proclamation has regulated the number of arbitrators, appointment of arbitrators and the rights and obligations of arbitrators in a more extensive manner than what was provided under the Civil Code. The parties are free to determine the number of arbitrators, but it must always be odd in number, and the manner of appointment of arbitrators has also been regulated. Foreign arbitrators can also be appointed by the parties to arbitrate disputes. The Proclamation also defined the rights and obligation of the arbitrators and set out some prohibitions such as individual meeting with the party or receiving gifts. An objection against the appointed arbitrators can be made by the parties to the tribunal and in case the objection is rejected by the tribunal, the matter can be referred to a court.

Removal of an Arbitrator; under the Civil Code, parties who want to remove an arbitrator owing to his default to discharge the obligations may request a court for the removal of arbitrators. Under the Proclamation, removal of an arbitrator can be done by the agreement of the parties in the event when the arbitrator failed to discharge his obligation. The parties are required to notify the tribunal for the latter to take a measure for the removal. Any grievance by the parties relating to the decision of the tribunal on the removal of an arbitrator is appealable to the Federal First Instance Court.

The Establishment of Arbitration Centres: The other new introduction is that the Proclamation permits the establishment of arbitration centres by government authority or private persons. The Federal Attorney General is empowered to license and supervise arbitration centres and set a criterion for their establishments without affecting the operation of existing centres.

The Recognition of the Kompetenz-Kompetenz Principle: The Proclamation recognizes that the arbitration tribunal designated by the parties have a power to determine the existence or nonexistence of a valid arbitration agreement and whether the tribunal itself has a jurisdiction to preside over the matter. To this effect, the Proclamation recognizes that the arbitration agreement will remain operational irrespective of the fact that the main contract becomes null and void. This limits an ill intended party from bringing the matter before courts by objecting the jurisdiction of the tribunal. It is only after the decision of the tribunal on its own jurisdiction that the party may bring the matter before Federal First Instance Court. Under the Civil Code, only the contracting parties are expected to authorise the arbitrator to decide disputes pertaining to jurisdiction.

The Taking of Interim Measures by the Tribunal: The other major departure of the Proclamation is that it expressly permits arbitration tribunals to take an interim measure and provides the conditions under which the measures can be issued. Upon the consent of the parties or on its own initiative, the Tribunal is authorised to take various preventive interim measures such as rendering decisions that properly preserve and maintain goods in dispute or assets and finds that on which an arbitration decision may be given. Any interim measure provided by arbitrators are binding in Ethiopia regardless of the place where the measure was issued. The parties are also free to require the court for the issuance of interim measures.

Proceedings of the Arbitration: the Previous Laws used to provide that the procedure of arbitration needs to be as near as the procedure of a civil court. The Proclamation deviated from this and has established the manner of setting the arbitration proceeding in motion, the service of arbitration notice, statement of claim and summon and their respective timing. The Proclamation also recognized the equal treatment of the parties in the arbitration proceeding, their freedom to determine the applicable procedural law and language of the arbitration. The manner of setting in motion the arbitration proceeding is by a notice to be submitted by the plaintiff and the manner of serving the notice to the other party is clearly regulated, which was not the case under the previous laws. The plaintiff is also expected to present a statement of claim with all the supportive evidences and the defendant shall bring a response for the allegations. The oral proceeding follows the written arguments which is discretionary to the tribunal. The tribunal may even request expert opinion on a particular issue of fact and it may also request for the support of a court in receiving evidence.

Arbitral Awards: the tribunal is expected to apply Ethiopian substantive law for resolving the dispute. If there are no such agreements, the tribunal has the jurisdiction to apply a law relevant to the matter. The Proclamation regulated the form and content of the arbitral award. Even after making the award, the tribunal is authorized to make the necessary correction on minor errors, provide interpretation or render an additional decision that is based on the application of one of the parties or on its own initiative.

Objection to and Appeal from the Arbitral Award: The Proclamation permits any third party whose interest has been affected by an arbitral award to lodge an objection against the award to the relevant court with a jurisdiction within 60 days. In principle, the Proclamation does not allow an appeal from the award unless parties agreed otherwise. However, unless the parties agreed otherwise, the parties are free to lodge an appeal to the Cassation Division when there is fundamental error of law.

The Setting aside of Arbitration Award: The Proclamation recognized the manner in which an arbitration award can be set aside. There is exhaustive list of grounds in which a court may set aside the arbitration award. This includes the incapacity of the parties to arbitration, the arbitration agreement becoming null and void, one of the parties not having an equal right to participate in the proceeding, when the arbitrators received a bribe or acted in a way that affected their independence and impartiality or when the tribunal acted without having jurisdiction or exceeded what transpired under the arbitration agreement.

Recognition and Execution of an Arbitral Award: As a principle, the Proclamation underlines that an arbitral award rendered in Ethiopia or abroad will be executed on the basis of the Civil Procedure Code as though the decisions were rendered by a court. An objection to the enforcement of an award can be made by a party on grounds that are similar with those grounds for setting aside the arbitration itself. With regards to foreign arbitral awards, the United Nations Convention on the Recognition and Enforcement of Foreign Arbitral Awards to which Ethiopia is a party would be applicable as long as the arbitral awards fall under the Convention. However, the Proclamation lists grounds by which a foreign arbitral award may not be enforced, which are similar in essence with the requirements provided under the Civil Procedure Code.

CONCILIATION

The Proclamation also regulates matters relating with conciliation. It defines conciliation as a process of dispute settlement that is facilitated by a third party designated by contracting parties in order to resolve existing or future disputes. The conciliator will be appointed by the parties themselves.

The Civil Code had only 7 provisions with regards to conciliation, while the Proclamation has become more elaborative and has 26 provisions. The basic new introductions are:

- A conciliation agreement that is validly made can be brought before a court as a preliminary objection;

- The Proclamation governs the formal process of initiating the conciliation proceeding, which is by the request of one party and the acceptance by another;

- The Proclamation provides the number of conciliators to be one, unless the parties agreed otherwise;

- The roles of the conciliator are expanded, authorising the conciliator to summon witnesses, hear expert opinion or conduct other activities. It also entrusts the conciliator to forward a proposal for conciliation;

- The Proclamation also provides that the conciliation proceeding is not required to be bound by any substantive or procedural laws;

- The Proclamation recognizes that a conciliation agreement shall remain confidential;

- It also allows parties to request an interim measure from courts while the conciliation proceeding is pending;

- When the parties agreed to the proposal of the conciliator, the conciliator will prepare a settlement agreement to be signed by the parties. Once the settlement agreement is drawn and agreed, it constitutes a final and non-appealable decision on which an application for execution can be submitted with a court of jurisdiction;

- The Proclamation permits parties to resort to court or arbitral proceedings when the conciliator failed to perform their obligations within the time agreed or within six months, if no time is set, or it provides a written declaration confirming that the dispute cannot be resolved through conciliation;

- One of the parties may apply to a court for the invalidation of the settlement agreement provided that the settlement agreement is null and void, lacks clarity, is contrary to public policy and peace, or the parties lack capacity to conclude the agreement;

- The Proclamation also introduced basic prohibitions and limitations. For example, the conciliator cannot serve as an arbitrator, attorney, or agent, or be a witness in any judicial or arbitration proceeding on a similar matter he handled as a conciliator. The suggestion forwarded or an admission made by one of the parties or a settlement proposal of the conciliator in the conciliation proceeding are inadmissible in judicial or arbitral proceedings; and

- With a bid to encourage parties to resolve their dispute through conciliation, the Proclamation offered the reimbursement of court fees paid by parties while instituting a court case when they have resolved their dispute withdrawing the court suit.

Disclaimer: This information is intended as a general overview and discussion of the subjects dealt with. The information provided here was accurate as of the day it was posted; however, the law may have changed since that date. This information is not intended to be, and should not be used as, a substitute for taking legal advice in any specific situation. Mehrteab Leul & Associates is not responsible for any actions taken or not taken on the basis of this information. Please refer to the full terms and conditions on our website.

Copyright©2021 Mehrteab Leul & Associates. All rights reserved.

Tuesday, 16 March 2021 07:47

The National Bank of Ethiopia’s New Directive on Retention and Utilization of Foreign Currency Earnings from Export and Inward Remittance (09 March 2021)

Written by Getu ShiferawThe National Bank of Ethiopia Issued a New Directive (Directive No. FXD/70/2021, New Directive) governing the retention and utilization of foreign currency earnings from export and inward remittance. Previously the area was regulated by the Directive No. FXD/66/2020 (Old Directive).

The basic changes introduced by the New Directive are highlighted below:

- Retention Account “A” and Retention Account “B” has been eliminated: under the Old Directive Exporters of Goods and Services and Recipient of Inward Remittance (Beneficiaries) were allowed to credit 30% of their foreign currency in Account A and hold for an indefinite time. 70% of the earning will be credited to Account B for 28 days only. The earnings were allowed to be utilised by the beneficiary for the importation of raw materials or other permitted items relating to the export business. Under the New Directive these two kinds of accounts are eliminated and only one Forex Retention Account is permitted.

- Mandatory Surrender is established: under the New Directive all the beneficiaries are required to surrender 30% of the foreign currency earning to the commercial banks. Previously there was no surrender requirements applicable to the Beneficiaries.

- The Amount of Proceeds to be Retained is reduced: the Beneficiaries are further required to sale 55% of the foreign currency earning to the bank immediately on the day of receipt at the prevailing buying exchange rate. The Beneficiaries can deposit 45% of the proceeds in retention account for an indefinite time. Note that this 45% shall be calculated once the 30% surrender is made on the total earnings.

- The requirements for utilization of the foreign currency has been changed: under the Old Directive the foreign exchange under retention accounts can only be used to finance direct business relating to the export and some other permitted payments. Under the New Directive the Beneficiaries are allowed to use the foreign exchange for the importation of goods and services without restriction as long as it has a business license to import these goods and services.

- A New Penalty is imposed on Banks: any bank that violates any provision of the directive is liable to pay 5,000 USD for each violation.

Disclaimer: This information is intended as a general overview and discussion of the subjects dealt with. The information provided here was accurate as of the day it was posted; however, the law may have changed since that date. This information is not intended to be, and should not be used as, a substitute for taking legal advice in any specific situation. Mehrteab Leul & Associates is not responsible for any actions taken or not taken on the basis of this information. Please refer to the full terms and conditions on our website.

Copyright©2021 Mehrteab Leul & Associates. All rights reserved.

Monday, 26 October 2020 22:14

The EPHI’s Latest COVID-19 Directive (Directive No. 30/2020)

Written by Ayele WoubshetAs an institution that is mandated to protect and promote the health of the Ethiopian people, the Ethiopian Public Health Institute (EPHI) has recently issued a Directive that seeks to mitigate the  growing spread of the Novel Coronavirus. Entitled A Directive Issued for the Prevention and Control of the COVID-19 Pandemic (Directive No 30/2020), this new Directive is expected to not only have serious implications for international travelers but also for those employers, employees and customers of local businesses. As such, this legal update will be exploring Directive No 30/2020 in light of the new changes it has brought about as well as explore its legal implications for those that are conducting business in Ethiopia.

growing spread of the Novel Coronavirus. Entitled A Directive Issued for the Prevention and Control of the COVID-19 Pandemic (Directive No 30/2020), this new Directive is expected to not only have serious implications for international travelers but also for those employers, employees and customers of local businesses. As such, this legal update will be exploring Directive No 30/2020 in light of the new changes it has brought about as well as explore its legal implications for those that are conducting business in Ethiopia.

After coming into effect in October 5 2020, Directive No 30/2020 has laid down a set of new requirements for those international travelers that wish to enter the country through its international airports. Beyond requiring travelers to provide a negative RTPCR test that was conducted up to five days before arrival, the Directive also requires international travelers to quarantine at home for seven days. This is in stark contrast with the previous Directive, which not only mandated international travelers to quarantine at home for fourteen days but also required them to present a negative RTPCR test that was conducted up to three days before arriving in Ethiopia.

Despite this, there has been a recent practice of not requiring international travelers to self-isolate so long as they have a negative RTPCR test and show none of the COVID-19 related symptoms. In contacting the EPHI for clarification, a representative of the Institute has informed MLA that the policy of home isolation, as per Part 4 of Directive 30/2020, is no longer being followed by the Ethiopian government for such travelers.

However, although Directive No 30/2020 has set a new policy for those international travelers that have tested negative for the Novel Coronavirus, the Directive has continued the policy of temporary isolation for those international travelers that display any of the symptoms associated with COVID-19. As such, regardless of their negative RTPCR test, international travelers that have a fever, headache, cough, loss of taste and smell, throat swelling, or any other related symptoms will still be taken to one of the temporary isolation centers that have been prepared by the government.

However, although Directive No 30/2020 has set a new policy for those international travelers that have tested negative for the Novel Coronavirus, the Directive has continued the policy of temporary isolation for those international travelers that display any of the symptoms associated with COVID-19. As such, regardless of their negative RTPCR test, international travelers that have a fever, headache, cough, loss of taste and smell, throat swelling, or any other related symptoms will still be taken to one of the temporary isolation centers that have been prepared by the government.

Apart from setting the standard for border health control, it is important to note that Directive No 30/2020 also goes a long way in regulating how private enterprises will be interacting with their employees as well as their customers. For example, the Directive obligates employers to not only provide precautionary materials to their employees but to also make information about COVID-19 readily available as well as ensure that employees are able to work whilst maintaining a safe distance between each other. This obligation to create a safe work environment is particularly stringent in the industry, construction and production sectors, where employers are also mandated to rearrange the workplace in a manner that will allow for physical distancing and sufficient air circulation. As such, by mandating employers to provide sanitary materials at their gates as well as ensuring that the workplace is in line with the public health guidelines of physical distancing and mask wearing, it is safe to say that Directive No 30/2020 provides a robust legal framework that accounts for the safety of employees.

Similarly, a business’s obligation to create a healthy and safe environment also affects how a particular business interacts with its customers, as they have a dual responsibility to protect both their employees and their patrons. In this light, Directive No. 30/2020 strictly prohibits the provision of services to those customers that are not maintaining a two meter distance or not wearing a mask. Moreover, businesses must ensure that sanitary materials are readily available for customers, that employees are wearing masks at all times, that anything used by customers are thoroughly disinfected, and that physical distancing guidelines are maintained by not sitting more than three customers at a single table and marking spots where customers could stand. In addition to these, it is worth noting that Directive No. 30/202 makes a clear distinction between service providers, as it mandates cinemas, galleries and theatres to ensure that their service rooms have adequate air ventilation and that their occupancy does not exceed one-fourth of their maximum occupancy capacity.

Apart from these, Directive No. 30/2020 has also established strict guidelines for those that wish to organize meetings and conferences in Ethiopia.  According to Part 5 of the Directive, meetings of up to fifty people can be held without an additional permit so long as the hall is well ventilated, attendees are able to maintain a distance of two meters between each other and the meeting does not take up more than one-fourth of the hall’s holding capacity. Furthermore, meeting organizers must prohibit participants without a face mask from entering the hall, provide sufficient sanitary material for attendees and keep a register of the attendees’ names, phone numbers and addresses for fourteen days. However, meetings with more than fifty attendees require a special permit from the Ministry of Peace as well as other peace and security structures at the regional, zonal and woreda levels.

According to Part 5 of the Directive, meetings of up to fifty people can be held without an additional permit so long as the hall is well ventilated, attendees are able to maintain a distance of two meters between each other and the meeting does not take up more than one-fourth of the hall’s holding capacity. Furthermore, meeting organizers must prohibit participants without a face mask from entering the hall, provide sufficient sanitary material for attendees and keep a register of the attendees’ names, phone numbers and addresses for fourteen days. However, meetings with more than fifty attendees require a special permit from the Ministry of Peace as well as other peace and security structures at the regional, zonal and woreda levels.

All in all, the directives found in Directive No. 30/2020 have significant implications for local businesses as well as those international travelers that wish to do business in Ethiopia. Given its new quarantine policy for international travelers, its policy for meeting venues as well as its clear workplace guidelines for employers, employees and customers, the EPHI’s new Directive provides a robust legal framework for businesses to operate whilst mitigating the spread of COVID-19.

More...

Friday, 16 October 2020 06:48

The NBE’s New Directive on Forex Allocation and Management (Directives No. FXD/67/2020)

Written by Getu ShiferawAs an institution that seeks to foster a healthy financial system as well as facilitate the rapid economic development of the country, the National Bank of Ethiopia (the “NBE”) has the power to formulate and implement those exchange rate policies that can help create a strong and stable economy. Whether it is by monitoring the foreign exchange transactions of banks, establishing the terms and conditions for foreign exchange transfers, or identifying those economic sectors that warrant the prioritized allocation of foreign currency, the role of the NBE in ensuring the efficient allocation of this important yet scarce resource cannot be overstated. This is particularly true in 2020, where the growing spread of the Novel Coronavirus and the troubling desert locust infestation has necessitated the reprioritization of Ethiopia’s decreasing foreign reserve coverage.

It is in this context that the new Transparency in Foreign Currency Allocation and Foreign Exchange Management Directives (“Directives No. FXD/67/2020”) came into effect in 05 October 2020. In doing so, there are some notable differences between Directives No. FXD/67/2020 and the Transparency in Foreign Currency Allocation and Foreign Exchange Management (as Amended) (“Directives No. FXD/62/2019”), particularly when it comes to how banks prioritize, allocate and utilize their foreign currency reserves. As such, this legal update seeks to assess the NBE’s recently issued Directives No. FXD/67/2020 in light of the previous Directives that regulated the allocation and management of foreign currency in Ethiopia.

It is in this context that the new Transparency in Foreign Currency Allocation and Foreign Exchange Management Directives (“Directives No. FXD/67/2020”) came into effect in 05 October 2020. In doing so, there are some notable differences between Directives No. FXD/67/2020 and the Transparency in Foreign Currency Allocation and Foreign Exchange Management (as Amended) (“Directives No. FXD/62/2019”), particularly when it comes to how banks prioritize, allocate and utilize their foreign currency reserves. As such, this legal update seeks to assess the NBE’s recently issued Directives No. FXD/67/2020 in light of the previous Directives that regulated the allocation and management of foreign currency in Ethiopia.

One important change brought about by Directives No. FXD/67/2020 is the downgrading of particular payments that Directives No. FXD/62/2019 not only considered to be important for foreign investors but also economically essential; warranting the prioritized allocation of foreign currency. In downgrading profit and dividend transfers as well as the transfer of excess sales of foreign airlines from Second Priority payments to Third Priority payments, the NBE has reverted to its 2018 position of considering these payments less of a priority than those other goods and payments listed in 6.1(a) and 6.1(b) of the Directive.

Although the recently enacted Investment Proclamation No. 1180/2020 states that any foreign investor has the right to not only remit the profits and dividends accruing from their investment but also those proceeds from the sale of the business or the transfer of shares, Directives No. FXD/67/2020 will likely make such transactions lengthy as the allocation of foreign currency is not only based on prioritized categories but also on a first come first serve basis. As such, even though Directives No. FXD/67/2020 requires banks to allocate 45% from half of their foreign currency reserves for all imports of goods and services to Third Priority imports and payments, the NBE’s first come first serve policy as well as the fourteen other payments and imports in this category will likely result in the diminished availability of funds for these two important transactions.

Although the recently enacted Investment Proclamation No. 1180/2020 states that any foreign investor has the right to not only remit the profits and dividends accruing from their investment but also those proceeds from the sale of the business or the transfer of shares, Directives No. FXD/67/2020 will likely make such transactions lengthy as the allocation of foreign currency is not only based on prioritized categories but also on a first come first serve basis. As such, even though Directives No. FXD/67/2020 requires banks to allocate 45% from half of their foreign currency reserves for all imports of goods and services to Third Priority imports and payments, the NBE’s first come first serve policy as well as the fourteen other payments and imports in this category will likely result in the diminished availability of funds for these two important transactions.

Another notable change brought about by Directives No. FXD/67/2020 is its specificity on who can request for special priority allocation of foreign currency. Whilst Directives No. FXD/62/2019 merely stated that the Governor or Vice Governor of the NBE may give special priority approval on a case by case basis, Directives No. FXD/67/2020 limits the discretion of both the Governor and Vice Governor by listing financial institutions, the federal government, regional governments, and city administrations as those that can request for special priority.

Although it is possible to infer from Directives No. FXD/67/2020 that financial and governmental institutions have supplanted investors when it comes to making such special requests, it is important to note that most of the essential imports are still prioritized for foreign exchange allocation. For example, pharmaceutical goods such as medicine and laboratory reagents continue to be classified as first priority essential goods that banks are now mandated to allocate 10% of their foreign currency reserves to.

Similarly, inputs for agricultural and manufacturing investments are still designated as secondary priority imports, making access to foreign currency relatively easier for those investors that wish to purchase and import fertilizers, seeds, and pesticides as well as manufacturing chemicals and raw materials. With Directives No. FXD/67/2020 also entitling bank presidents to approve the import of spare parts for those faulty machinery that can disrupt production, it is our opinion that Directives No. FXD/67/2020 is more supportive of the manufacturing and agricultural sectors than the Directive it repealed.

Furthermore, foreign investors are already exempted from the registration process that underpins this priority scheme, as they are still afforded foreign exchange on demand for some of their fiduciary interests. Whether it is the repayment of the principal interest or fees of external debt obligations, the payment of suppliers’ credit, the repatriation of salary by foreign employees, or fees related to consultancy, commissioning and royalties, neither the limitation placed on special priority requests nor the de-prioritization of certain payments will hinder their ability to fulfill their fiduciary responsibilities to their creditors as well as their employees.

Furthermore, foreign investors are already exempted from the registration process that underpins this priority scheme, as they are still afforded foreign exchange on demand for some of their fiduciary interests. Whether it is the repayment of the principal interest or fees of external debt obligations, the payment of suppliers’ credit, the repatriation of salary by foreign employees, or fees related to consultancy, commissioning and royalties, neither the limitation placed on special priority requests nor the de-prioritization of certain payments will hinder their ability to fulfill their fiduciary responsibilities to their creditors as well as their employees.

In conclusion, the enactment of Directives No. FXD/67/2020 will likely make payments related to profit and dividend transfers as well as the transfer of excess sales of foreign airlines a lengthy process as the allocation of foreign currency is not only based on prioritized categories but also on a first come first serve basis. However, Directives No. FXD/67/2020 still affords foreign investors the right to obtain foreign exchange on demand for some of their most essential fiduciary responsibilities.

Disclaimer: This information is intended as a general overview and discussion of the subjects dealt with. The information provided here was accurate as of the day it was posted; however, the law may have changed since that date. This information is not intended to be, and should not be used as, a substitute for taking legal advice in any specific situation. Mehrteab Leul & Associates is not responsible for any actions taken or not taken on the basis of this information. Please refer to the full terms and conditions on our website.

Copyright©2020 Mehrteab Leul & Associates. All rights reserved.

Thursday, 17 September 2020 17:14

Legal Update: Ethiopia Passed New Investment Regulation

Written by Getu ShiferawIntroduction

The Ethiopian Government has made commendable efforts, through legislative and procedural reforms, to improve the investment climate of the country and thereby attract more foreign direct investment. Since 1992, the investment law has been revised four times to ensure the participation of more foreign investments in various sectors of the economy. The latest law, the Investment Regulations No. 474/2020 (the “Regulation”) was promulgated on 02 September 2020.

The Regulation, in a stark deviation from its predecessor has changed the “positive list” approach into a “negative list “. In the repealed Investment Regulation of 2012, foreign investors were only allowed to invest in sectors expressly listed in the investment regulation or in sectors opened by the decision of the Ethiopian Investment Board. The shift towards a ‘negative list’ is probably the most significant aspect of the new investment law because foreign investors are now allowed to invest in any investment area except those that are expressly reserved.

1. Major Amendments in the Regulation

1.1 Opening of Reserved/Restricted Sectors to Foreign Investment

One of the major change the Regulation has brought is the restoration of the “negative listing” of investment areas that are open to foreign investors which enables foreign investors to enjoy a much greater opportunity with regards to the areas that they can invest in. The negative listing approach employs the opening of all economic sectors to FDI except those that are expressly reserved/restricted by law. This approach aspires to cope with the ever-changing technological evolutions and pace of business in a globalized economic sphere. This approach is a reversal of the 2012 Investment Regulation which adopted the “positive listing” method that was restrictive by design.

As part of the negative listing approach, the Regulation provides three categories of investment areas. These are areas exclusively reserved for joint investment with government, areas exclusively reserved for domestic investors and areas exclusively reserved for joint investment with domestic investors. All other sectors not reserved in aforementioned sectors will be open for foreign investment.

1.1.1 Areas of investment that are open for foreign investment:

1.1.1.1 Electronic commerce;

1.1.1.2 Real estate development;

1.1.1.3 Education services;

1.1.1.4 Health services excluding primary and middle level health services

1.1.1.5 Grade 1 construction and drilling services;

1.1.1.6 Wholesale of petroleum and petroleum products and wholesale of own products produced in Ethiopia;

1.1.1.7 Import of liquefied petroleum gas and bitumen;

1.1.1.8 Cement manufacturing;

1.1.1.9 Capital goods finance business;

1.1.1.10 VAS (Value Added Services);

1.1.1.11 Management consultancy services;

1.1.1.12 Engineering consultancy services;

1.1.1.13 Repair and maintenance of heavy industry machineries and medical equipment;

1.1.1.14 Operating lease of industry-specific heavy equipment’s, machineries and specialized vehicles;

1.1.1.15 Star-designated national cuisine restaurant service;

1.1.1.16 Star-designated hotel, lodge, resort, motel, guesthouse and pension services;

1.1.1.17 Producing bakery products and pastries for export market;

1.1.1.18 Railway transport services;

1.1.1.19 Cable-car transport services;

1.1.1.20 Cold-chain transport services;

1.1.1.21 Freight transport services having a capacity of more than 25 tones;

1.1.1.22 Manufacturing;

1.1.1.23 Agro-processing and commercial farms;

1.1.1.24 Any investment activity that doesn’t fall under one of the below three categories (areas exclusively reserved for joint investment with government, areas exclusively reserved for domestic investors and areas exclusively reserved for joint investment with domestic investors).

1.1.2 Areas allowed for foreign investors to jointly invest with the government:

1.1.2.1 Manufacturing of weapons, ammunition and explosives used as weapons or to make weapons;

1.1.2.2 Import and export of electricity;

1.1.2.3 International air transport services;

1.1.2.4 Bus rapid transit; and

1.1.2.5 Postal services excluding courier services.

1.1.3 Areas of investment in which foreign investor/s can own up to a maximum of 49% of share capital:

A foreign investor jointly investing with a domestic investor (Ethiopian nationals or companies wholly owned by Ethiopian nationals) in the following areas can own up to a maximum of 49% of share capital of a joint venture company. These areas are:

1.1.3.1 Freight forwarding and shipping agency services;

1.1.3.2 Domestic air transport service;

1.1.3.3 Cross country passenger transport service using buses with a seating capacity of more than 45 passengers;

1.1.3.4 Urban mass transport service with large carrying capacity;

1.1.3.5 Advertisement and promotion services;

1.1.3.6 Audiovisual services; motion picture and video recording and distribution; and

1.1.3.7 Accounting and auditing services.

1.1.4 Areas of investment exclusively reserved for domestic investors:

1.1.4.1 Banking, insurance and microfinance businesses, excluding capital goods finance business;

1.1.4.2 Transmission and distribution of electrical power through integrated national grid system;

1.1.4.3 Primary and middle level health services;

1.1.4.4 Wholesale trade, excluding wholesale of petroleum and petroleum products and wholesale of own products produced in Ethiopia, electronic commerce;

1.1.4.5 Retail trade, excluding retail of and electronic commerce as provided under appropriate law, of own products produced in Ethiopia;

1.1.4.6 Import trade, excluding liquefied petroleum gas and bitumen;

1.1.4.7 export trade of raw coffee, khat, oil seeds, pulses, minerals, hides and skins, products of natural forest, chicken, and livestock including pack animals bought on the market;

1.1.4.8 Construction and drilling services below Grade I;

1.1.4.9 Hotel, lodge, resort, motel, guesthouse, and pension services, excluding those that are star-designated;

1.1.4.10 Restaurant, tearoom, coffee shops, bars, nightclubs, and catering services, excluding star-designated national cuisine restaurant service;

1.1.4.11 Travel agency, travel ticket sales and trade auxiliary services;

1.1.4.12 Tour operation;

1.1.4.13 Operating lease of equipment’s, machineries and vehicles, excluding industry-specific heavy equipment’s, machineries and specialized vehicles;

1.1.4.14 Making indigenous traditional medicines;

1.1.4.15 Producing bakery products and pastries for domestic market;

1.1.4.16 Grinding mills;

1.1.4.17 Barbershop and beauty salon services, smithery, and tailoring except by garment factories;

1.1.4.18 Maintenance and repair services, including aircraft maintenance repair and overhaul (MRO), but excluding repair and maintenance of heavy industry machineries and medical equipment;

1.1.4.19 Aircraft ground handling and related services.

1.1.4.20 Saw milling, timber manufacturing, and assembling of semi-finished wood products;

1.1.4.21 Media services;

1.1.4.22 Customs clearance service;

1.1.4.23 Brick and block manufacturing;

1.1.4.24 Quarrying;

1.1.4.25 Lottery and sports betting;

1.1.4.26 Laundry services, excluding those provided on industrial scale;

1.1.4.27 Translation and secretarial services;

1.1.4.28 Security services;

1.1.4.29 Brokerage services;

1.1.4.30 Attorney and legal consultancy services; and

1.1.4.31 Private employment agency services, excluding such services for the employment of seafarers and other similar professionals that require high expertise and international experience and network.

1.1.4.32 Transport services, excluding the following areas:

(a) Railway transport services;

(b) Cable-car transport services;

(c) Cold-chain transport services;

(d) Freight transport services having a capacity of more than 25 tones; and

(e) Transport services reserved for joint investment with the Government or domestic investors.

Disclaimer: This information is intended as a general overview and discussion of the subjects dealt with. The information provided here was accurate as of the day it was posted; however, the law may have changed since that date. This information is not intended to be, and should not be used as, a substitute for taking legal advice in any specific situation. Mehrteab Leul & Associates is not responsible for any actions taken or not taken on the basis of this information. Please refer to the full terms and conditions on our website.

Copyright©2020 Mehrteab Leul & Associates. All rights reserved.

Introduction

Since the appointment of its new Prime Minister (Abiy Ahmend) in 2018, Ethiopia has witnessed a series of broad ranging economic and legal reforms aimed at boosting the economy by encouraging foreign direct investment (FDI). In view of this, on February 13, 2020 the Ethiopian Government approved the ratification of the 1958 Convention on the Recognition and Enforcement of Foreign Arbitral Awards, commonly known as the New York Convention. In doing so, Ethiopia becomes the 33rd African and the 162nd international State to sign the New York Convention.

Implications on the ratification of the New York Convention

Ratifying the New York Convention is a significant step forward for Ethiopia and underpins the country’s ongoing efforts to attract greater foreign investment. The adoption of the uniform framework for the recognition and enforcement of arbitral awards will certainly help to improve the country’s profile as a business-friendly jurisdiction.

The previous regime1 for enforcement of foreign judgments and arbitral awards contained a number of grounds which were considered obsolete and ambiguous. The decision to adopt the New York Convention therefore provides international parties with greater certainty and brings the Ethiopian arbitration ecosystem into line with international standards.

One of the most significant stumbling blocks under the old system was the requirement for reciprocity to be demonstrated in order to enforce a foreign arbitral award. In other words, in order for a party to enforce a foreign arbitral award in Ethiopia, the party would have to show that the State where the arbitral award was made would recognize and enforce an arbitral award made in Ethiopia on the basis of reciprocity. As Ethiopia was not a party to the New York Convention, this rule meant that it was virtually impossible to enforce a foreign arbitral award in Ethiopia.